This blog post was written in collaboration between Devin Hunt, David Mytton, and the fearless editing of Nelson Casata. It was originally published on Medium.

I recently caught up with a long time friend, co-founder of Lyst, and Venture Partner at Seedcamp Devin Hunt about his view on the role of Product Manager. What followed was a fun deep dive into the evolving nature of the role, but also an exploration into its relative infancy in terms of what best practices are, and why this makes it challenging for founders looking to hire a PM to know what to look for. This blog post is a summarised and synthesised version of our chat, but hopefully it helps you answer the following questions:

First, let’s start by defining the role of a Product Manager (PM). A PM is more than just one thing, it’s a role that encompasses several disciplines. To make it simple, I’ve broken out those disciplines into four categories: Product Leadership, Management, Design, and Sales.

Leadership, in the context of being a Product Manager, means making the critical decisions based on your team’s research and the product vision set out by the founder. In our chat, Devin shared that there are two unique streams in building product: developing the product vision, and executing on it, which he calls product operations. Whereas a founder might be hyper critical in setting product vision (at least until they trust the PM), the product operations (think customer development, iterating on ideas, tech requests, etc) still require decision-making leadership.

Typically, the blend of leading product operations and marrying that up with the product vision of the founder is what defines the key leadership attributes of a PM, especially in younger startups.

In effect, the PM will become an arbiter between product vision and product operations. They will have to understand customer development and initially do it jointly with the founders, but later manage what success looks like.

Which brings us to *Management.* Within management, a good PM is able to manage the team that delivers and maintains the product. This ranges from managing the priority stacks from both the engineering and design teams, the customer service requests, and the like. In effect, this is where the core of the confusion sometimes happens around Product Managers being perceived as Project Managers. Clearly there is some overlap, but there is more to the role of a Product Manager, than simple Project Management.

Next, comes *Design*. Whilst some of the best designers in the world don’t have a formal education in design, it helps to have an eye for what is ‘quality’, particularly quality for your customer. The PM needs to know how to calibrate the trade-off between quality of the product shipped vs. the’ speed’ of shipping. The PM needs to be able to understand what good delivery and a good user interface looks like, but doesn’t need to be the one doing it. It’s not uncommon for a PM to start recruiting a design team to support in making those design decisions, and scale those design teams as further funding rounds come. Andy Budd will be publishing a series of deep dives on around design with us at Seedcamp over the next few weeks — stay tuned.

Finally, I added *Sales* as the last ‘wish list’ attribute. Ultimately as much as the title of the book by Daniel Pink is around ‘to sell is human’, I’d argue that to build a product is to build a product around human interactions. I wrote a piece a while ago on the relationship process and product cycle and feel that a PM benefits from understanding what customers need and want and a background in some form of sales can be handy. David Mytton, who we’ve been lucky to have as an EiR with us at Seedcamp for a few years, adds that the commercial element of a PM is largely overlooked: the full go-to-market strategy needs to go alongside product functionalities.

Now… How to find a PM? Well, one of the interesting observations Devin shared with me is that in a human resource constrained ecosystem (think Silicon Valley where lots of the PMs are hired by big tech firms), there have been many lateral hires that have ended up being good product managers with the right level of encouragement. As I explored with Devin what were the key attributes that stood out for a good PM, responsibility, trust, ability to manage and communicate, and organisation stood out as strengths over intrinsic ‘design’ skills or engineering skills, for example. As such, as you reflect on people in your network that could be PMs, don’t overlook ex-sales, ex-engineers, or ex-lawyers if they understand your segment & customer. They could very well be trained to be great PMs for your business.

To conclude, when is the best time to bring in a PM? As soon as you can afford to if you are a commercially minded CEO, and if you’re a technically minded CEO, likely still as soon as you can afford, although you can potentially get away with it for much longer provided you evaluate your role as not preventing you from leading the wider organization effectively.

In the words of David Mytton: The best founder teams have two people, one commercial and one technical. They’re the skills of a PM in two people. I think startups tend to grow the engineering teams out of line with the commercial, though they should be growing together. The PM sits across both. There’s a lot of logistics in customer development in the early days, so seed stage is probably around the right time to gear up those efforts.

On this subject, Alex from Forward Partners wrote in a recent blog post of this very point which I agree with. Read his blog post, it’s quite good.

“Typically a startup’s founder will fill the role of the Product Manager for the first 12 months. This is essential as every good founder should have an intimate knowledge of both their business goals and their customers. However as the founder takes on a more focused role as CEO of the company, she will have less time to manage the product and will instead start prioritising the strategic direction of the business. Constrained by budget and often encouraged to focus on hiring support around technology or growth, she will make do until the startup is at a large enough size that she is able to afford dedicated help with her product. Yet this can often be too late. By the time that your business has secured seed-stage or later funding the foundations of good product thinking (also referred to as having a good “Product Muscle”) should be well and truly in place. This should coincide with the first 12 to 18 months of your product’s lifecycle. Being able to present a deep and meaningful understanding of your customer to investors, along with a story of increased revenue due in large part to adapting the product to better serve your customer base, will go a long way in securing future investment. With this in mind, we believe that a Head of Product should be amongst the first key hires that you make during your first 12 months.”

I’ve put together a list of resources below, in various blog posts, books, podcasts and tools to dive in on further on the topic:

Blogposts:

Good Product Manager/Bad Product Manager

Product managers are not responsive for “how”

The Black Box of Product Management

Books:

Inspired: How to Create Tech Products Customers Love

The Lean Product Playbook: How to Innovate with Minimum Viable Products and Rapid Customer Feedback

Product Roadmaps Relaunched: How to Set Direction While Embracing Uncertainty

Podcasts:

The product podcast (Spotify)

Build with Maggie Crowley (Spotify)

Seedcamp Product Summit:

In this post, our Managing Partner, Carlos, provides an update and further considerations for founders questioning how an early-stage investor values a startup? If you want to know how to maximize your valuation and drivers behind the boundaries of possible valuations for your company then read on!

In my previous post, I covered how macro and geo contexts, amongst several factors, determine the relativistic value of a company to an investor on exit, and how traditional finance-driven valuations methods (DCF, etc) were inappropriate for early-stage startups even if some of the elements that drive those finance-driven valuation methods were still applicable, such as expected revenues. I also covered how several factors about your company can influence what valuation you might be able to achieve. To kick-off, let’s revisit those points.

The key drivers for maximizing your valuation possibilities are:

As I’ve written on metrics and FOMO before, I want to focus on the last three for this blog post.

In previous chapters I touched upon the basic fundraising equation:

[Money Raised / Post Money = % Dilution] or alternatively [Money Raised/% Dilution = Post Money], and “valuation” is typically used interchangeably used with “pre-money valuation” which is equal to [Post money – the Money Raised].

The key element to consider with the above equation is that it’s not static. The variables that make up the equation change with time. These changes create higher and lower ranges that are acceptable for investors and founders, and below, we’ll cover how those come into play in more detail.

As covered before, It all starts with macroeconomic conditions and general sentiment in public markets. When things are going well, all companies rise, the index of stocks in a country rise, valuations rise, and the tolerance for buyers and investors to invest more and at higher valuations also rises. With all of that on the rise, at the earlier stages, this manifests itself by investors being able to tolerate increasingly more ‘expensive’ rounds, as in, rounds where they have to pay a higher valuation because they see a possibility of selling their share of the company at a higher valuation in the future.

So, that’s the first point to make: in good times, investors are willing to increase post-money valuations. In bad times, this will no longer be the case, and if you want to read more on how to brace for that, I’ve covered it on how to weatherproof your business.

Secondly, the more mature the ecosystem, the more capital there is at play. As well as a greater volume of money, there will be more specialised and sophisticated investors who can better judge the potential and therefore may pay more. The more investors and money around the table, the more competitive deals get, which will affect your valuation for the better. This is why it is easier to raise money at a higher valuation in California vs. an emerging ecosystem.

These two factors above imply that there is no ‘static’ view of valuation, rather, it’s dynamic, as it is affected by externalities.

Taking the above into consideration, the more constructive way of thinking of valuation is by thinking of it as an ‘acceptable’ or ‘probable’ range relative to the amount of capital you are raising.

This range has an upper and lower boundary, which bookend what your valuation could be. From an investor’s point of view:

The UPPER %-dilutions boundary– no early-stage investor is looking to take a majority stake of your business as that would likely constitute an acquisition, so you can easily remove taking 50% of your company at a round off the table. Therefore, your ‘real’ upper boundary is usually imposed on the investor by a few factors out of their control, including the competitiveness of the local ecosystem, the options of capital available to the founder, and how much the investor cares about how they could be perceived by other investors (some investors don’t care if they come across as predatory).

The LOWER %-dilution boundary -no investor is likely to give you money for free. As investors compete for your deal, they will be more keen on offering you more money for less dilution to you, but there is a limit. As investors do internal calculations on what is the minimum they need to return an investment to their investors (based on macro-conditions and expectations of the future of your company), there is a point where they simply can’t make the numbers work for them and they usually opt-out of offering you a deal if an alternative offer at a higher valuation (lower dilution) comes into the offers the founders are considering. Investors that understand your industry better will naturally have more tolerance towards higher valuations (eg, lower % dilution) as they can see the future potential of the company more clearly.

From a founder’s point of view, therefore, it’s about pushing towards a lower boundary through the variables you can control, eg. metrics, fomo, and round size (more to cover later).

Even though the boundaries above seem like they provide an endless amount of options, it actually sets the stage for a way of thinking of your company’s value… as a ‘range’ of options relative to the amount of capital you are raising instead of as a ‘fixed’ value.

So what’s an acceptable range then? Well if the range is dictated by macro conditions, then surely there is some sort of rule-of-thumb? Luckily there is, but it’s confusing as its different for angels vs. institutional investors and with new types of investors coming online (eg. pre-seed investors) that just adds more to the mix. However, there is still a ‘range’ that you can use.

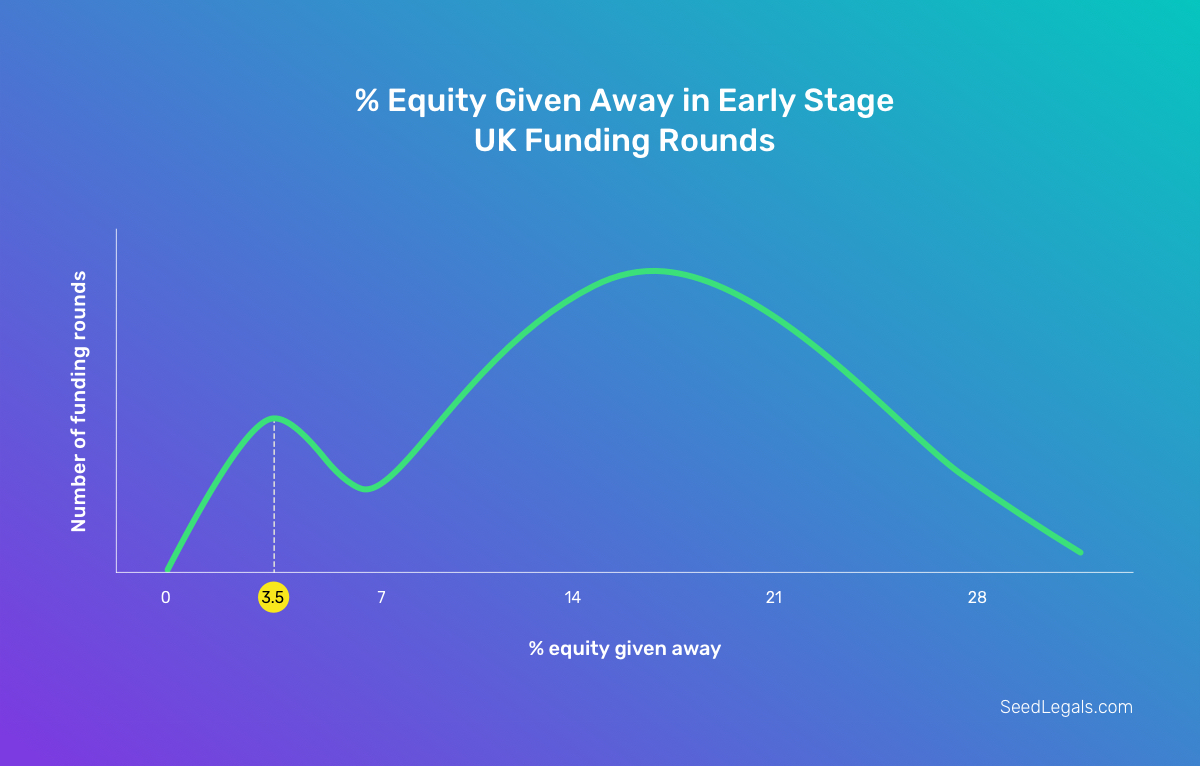

Seedlegals, a SC company, compiled some stats around valuations for pre-seed and seed rounds in the UK, for example, and this is the range they found (combined):

If you look at that gap (the tighter bit of it) and you say that it’s between 12% and 3.5% at the pre-seed stage and 25% to 12% to at the seed stage, you see that on average the ‘spread’ between the lower and upper boundaries on average is about 10%. To put that in context, if you were raising a 1m seed round, that would be the difference between a 3m valuation and a 7m valuation. Yes, it means a lot, but it also helps provide you with a workable range, and helps you contextualize what might be possible within ‘the norm’ (excluding crazy metrics or fomo).

However, the 5th point I brought up that affects your valuation is the round size you go out to raise. As you can see, if I take the same range of dilution of 25%-12%, then a 2m round would generate a valuation range of 7m-15m. Quite the jump right? Simply put, as you can’t control the macro factors that determine the range you operate in, as a founder, you have total control over your round size, which is your primary tool in changing your valuation, along with showcasing strong metrics and developing the factors that can generate FOMO for your industry.

But It’s not simply about increasing your round size to exact the valuation range you want.. You will be evaluated for investment on what you’ve achieved and how you will effectively use the funds raised, so there is a point, where investors may very well think you’re raising too much for where you are, and that will be subjectively up to the discretion of the investor relative to your industry (and the implied valuation that that amount of cash will imply for them, more on that below).

In conclusion, you can’t control macro-economic conditions nor can you control how upper and lower boundaries change over time for investors, but you can control how much you are raising, and that affects your valuation just as much.

Extra Geek Math on how to find a round size range based on the above – If you want to figure out what a probable round size for your company could be, AngelList host a valuation range by $ here – https://angel.co/valuations Mapped with the % dilution range from Seedlegals, you can backwards solve for what acceptable ranges might be. For example, for London, AngelList’s calculator says that the average valuation is $3.3m. If you assume that represents the pre-money and you solve for round-size, assuming the range of between 25% and 12% as per the above examples, and with some algebra to solve for round size, you end up with a viable round size of between $680K and $1.6M on average as per the data. Can you do better than that? For sure, but now you know how to calculate it!

Special thanks to our Venture Partners, Devin Hunt & Stephen Allott, for helping me proof-read this post!

This article was written by Carlos Espinal, Partner at Seedcamp – Europe’s leading Acceleration Fund. Providing up to $250k capital and access to its Academy learning programme, startups also have access to an active network of Europe’s top mentors and investors.

This article was written by Carlos Espinal, Partner at Seedcamp – Europe’s leading Acceleration Fund. Providing up to $250k capital and access to its Academy learning programme, startups also have access to an active network of Europe’s top mentors and investors.

Across society there is an increasing trend of experiences eclipsing that of owning material goods. We’re seeing this trend increasingly in action around the globe.

Some articles (U.S.News via Yahoo / Fast Company / NPR) have explained why millennials, for example, are choosing to live for experiences and less for ‘things’ (or at least the ownership of things). If and when they do buy things… there is a trend to buy things that have stories behind them and things that are longer-lasting. While the generational explanation helps explain an increase in some services and products, other articles simply point to economic stagnation as a main catalyst for the growth of the sharing economy. Economic concerns have also affected the luxury goods demand from Russia and China.

In addition to generational trends and economic circumstances, increasingly popular sociological movements like the tiny-house movement and the minimalism movement are promoting a simplified life that focuses on doing vs owning – and if you do own, have it be something that you’re likely to get value out of for a while (thus forcing a view towards higher quality affordable goods that don’t make you feel like they have designed obsolescence nor are about showing off).

Taking these trends into consideration, at Seedcamp we’re bullish on startups that bring experiences, meaning, convenience, and quality durable products to the market and/or allow for people to share products they own (enabled by tech to help them scale).

Below, is a list of Seedcamp companies that enable and participate in this trend:

Seedcamp Developer Ninja

If you’ve always wanted to hack with some of the best startup companies in Europe, here’s your chance. Seedcamp is looking for a full-time hacker-in-residence. Apply via this link.

It goes without saying that you’ll have a chance to chat with Seedcamp Founders if they’re stuck on stuff, and you’ll play an integral role within the Seedcamp team in helping set our tech strategy. Yes, it’s a lot of moving parts, but we are looking for rockstars who love tech and want to make a difference for the ecosystem.

We look forward to hearing from you!

The Job

Help develop our online products and strategy

Lead and manage all current online products and determine the best way to integrate them for most effective work by the team

Extract and analyse Seedcamp startups data and that of the general ecosystem

Work closely with the Head of Content and the Seedcamp Team to ensure that all online content, social media and work product takes the best advantage of tech know-how

Help research technology trends and assist with due diligence

Work from time-to-time with Seedcamp startups on some of what they need

About You

Comfortable with HTML, CSS, Javascript, & PHP.

Ideally comfortable (or at least an interest in learning) with Symfony2 (php framework), RoR, & postgres.

Ideally also have *nix sys-admin experience

Live and breathe technology and startups and are passionate about empowering founders and growing the startup community.

Self-driven, resourceful & results oriented – ready to roll up your sleeves and think creatively.

Thrive working under pressure, you’re organised and can multi-task, creating awesome, accurate content quickly.

Can interact with, and help manage, a creative, fast-paced and fun team.

Have experience working in startup environment, you have solid knowledge about marketing, growth and product as relevant for startups.

Ability to communicate verbally and written across both technology and business teams

Strong time-management skills.

Experience collecting and analysing media metrics – you can data crunch with the best of them.

Bonus Points

You ultimately want to do your own startup or join an early stage business

You can already amaze us with dev work you’ve done

To apply for the role please upload an up-to-date copy of your CV with a short covering note. Be sure to include links to your work to show us how awesome you code and hacker you are.

Questions: careers [at] seedcamp.com

Apply via this link.

We are very happy to introduce StrategyEye as one of our most recent additions to the Seedcamp Founders’ Sponsors. Seedcamp company CEOs will gain access to StrategyEye’s Digital Media platform for a full year and StrategyEye will also be regually publishing interviews with Seedcamp CEOs. Below is StrategyEye’s ‘Hot Company Profile’ on, Seedcamp company, Futurelytics.

Big data is big business at the moment. And while Futurelytics concentrates on small-to-medium-sized businesses and emphasises the importance of relevance when it comes to customer analytics, rather than simply the size of data sets, potential customers will perceive its offering as a big data solution. The firm recently won funding at Seedcamp Budapest and CEO Daniel Hastik is now aiming to make an impact by selling to sales and marketing teams in the US.

Big data is big business at the moment. And while Futurelytics concentrates on small-to-medium-sized businesses and emphasises the importance of relevance when it comes to customer analytics, rather than simply the size of data sets, potential customers will perceive its offering as a big data solution. The firm recently won funding at Seedcamp Budapest and CEO Daniel Hastik is now aiming to make an impact by selling to sales and marketing teams in the US.

¤ What differentiates Futurelytics from similar services?

It is a data mining solution. We connect marketing and sales guys, giving them information about customers by tracking data from multiple sources and scoring the customers from the best to the worst based on various parameters. We then group these customers’ information into segments so the guys in marketing and sales can use targeted campaigns. We also pull the data from our platform to marketing automation systems like MailChimp and Marketo.

We take the best practises and visualise the data and work with companies automatically so that the end user doesn’t have to make any major decisions. We tell them what will work and that’s the major difference. For example, we could say ‘in order to get churn customers back to you, you should do this’. Our team has a background in business analytics, so we are looking for meaningful patterns in the data. It doesn’t matter if it is just two rows in Excel, if someone doesn’t understand it then it’s the same if he has five terabytes of data that he doesn’t understand. We give the user what we think is important and what is not. Other companies focus on the size of the data and not the relevancy.

¤ What is your business model?

We make money in three different ways. One is a monthly subscription model for the platform itself, which is USD450 per month. The second revenue stream is our independent app on a CRM marketplace, for example Salesforce’s App Exchange. The third is license fees for what we call ‘powered by Futurelytics’. We are negotiating with certain CRM providers to embed our functionality.

¤ Who are your main competitors?

One would be Custora and the other one would be Cloud9. There are obviously the big players like SPSS from IBM, but that’s not the segment for our customer reach, we don’t go up into the enterprise we stay with small-to-medium sized businesses.

¤ What’s the biggest challenge you currently face?

We are a US-based company, but all the guys are in the Czech Republic at the moment, with one sales guy in the UK. For most businesses to set up in the US you need to be a US citizen so it’s quite difficult for European startups without having a US citizen in the team to actually start a business in the US.

The other challenge is getting the word out, so the marketing and sales, which we have not tracked as well as we do the technical side. We are now looking for people who can help us with that and that’s one of the reasons we joined Seedcamp. Their network, their knowledge and their companies within their investment team solved the same problems we are facing. So we are sharing a lot of information and that has been really helpful.

¤ What do you think is the hottest trend in digital media?

Competition between the stable, TechCrunch-like blog styles against blogs for particular technologies, which shift from the more mainstream to specific technologies. I am finding more information from our competitor’s blog than on GigaOm, for example.

VERDICT

The demand for big data services is booming. The market will be worth USD18.2bn this year before climbing to USD47.8bn in 2017 and analytics applications revenue is forecast to be the fastest-growing segment in the next four years, with revenues expected to increase by nearly 300%. Services such as Futurelytics, which promise to decipher the reams of online information and present actionable strategies from it, offer obvious tangible benefits for companies and salespeople. IBM expects its overall business intelligence revenue alone to come in at USD25bn by 2015, with plenty of dollars available to those that can gain scale quickly.

The main challenge for Futurelytics is standing out in an already overcrowded space. As well as startups such as Custora and Cloud9, big guns like Accenture and IBM are trying their hand at customer analytics. While Hastik maintains that the likes of IBM are after the big enterprise customers, where it is after small businesses, it doesn’t seem a stretch for IBM to scale out to SMEs. Futurelytics needs to make sure it can build out its offering quickly and expand rapidly to new markets.

The other issue is its current focus on the US. Hastik already concedes that it is struggling to expand, with problems setting up its services in the US hampering progress. Plenty of homegrown competition will continue to emerge stateside, while Futurelytics deals with these challenges. The firm also doesn’t disclose financial information, making it hard to ascertain how things are going in markets where it is available. It is important to note that it’s still early days, with the firm only launching in September. And it does already have 25 clients on board, including brands such as Yamaha, Time Warner Cable and Livestrong. As a result, the firm is “just starting” to generate revenue and the next six months will prove crucial for the startup.

AT A GLANCE CEO: Daniel Hastik HQ: Delaware, US Founded: September 2012 Employees: Six Commercial launch: September 2012 Funding to date: EUR50,000 (USD67,000) Investors: Seedcamp

COMPETITORS Custora

Hello Berlin! Next week we are kicking off our second full-blown Seedcamp Week of the year, this time in the German startup epicentre, Berlin. Applications flooded in from all over and made for a high calibre selection pool. This event also marks the first Seedcamp Week that winning teams from our Mini Seedcamps will participate in the competition to be part of the Seedcamp Family. Seven of the twenty teams that will be joining us in Berlin first met Seedcamp at a Mini Seedcamp in their home country; one from Mini Seedcamp Belgrade, two from Mini Seedcamp Kiev, one from Mini Seedcamp Istanbul, one from Mini Seedcamp Tel Aviv and two from Mini Seedcamp Stockholm.

We will be joined by Entrepreneurs, Product and Marketing Experts and some of the best operators across the German and European startup scene for the Mentoring Day on Tuesday at The Wye. Demo Day will follow on Wednesday at BDMI and will feature winners of the Seedcamp event. The event will also showcase some of our earlier Seedcamp teams who are currently fundraising. We have invited the top investment funds across Europe to attend, including investors from Index Ventures, Point Nine Capital, Balderton Capital, BDMI, Earlybird, DFJ Esprit and T-Venture.

Please meet the teams that will be participating at Seedcamp Week Berlin and check out the great things they are doing:

We are very thankful to our Event Partner in Berlin, BDMI, who make this event possible, and we would also like to thank our venue hosts in Berlin: The Wye, BDMI, and The Factory, who will be hosting a BBQ on Tuesday night. And, last but not least, another big thank you to the Seedcamp Sponsors: Google, Microsoft BizSpark, Nokia, Barclays, Qualcomm Ventures and PayPal Developer.

This is a guest post written by Yalim K. Gerger, Founder of Formspider, our Event Partner for Mini Seedcamp Istanbul on the 30th of April.

”If the whole world was a state, Istanbul would be the capital of it.” – Napoleon

Throughout its 3000 year history, Istanbul has hosted kings, sultans, queens, presidents, popes, an UEFA Cup Final, a historic Champions League Final, World Basketball Championships, Formula One Racing, Guns N’ Roses, Madonna, Michael Jackson and James Bond…Yet this global city has not, to this day, hosted a single Seedcamp event.

This is about to change.

On April 30th, the inaugural Mini Seedcamp Istanbul event will be held at the ITU University Maslak Campus KSB Auditorium.

Turkey has a fledgling startup community with over 200 companies registered on AngelList. Its ecosystem of entrepreneurs, VC’s, incubators, mentors and angels is growing quickly. There are plenty of national and international success stories such as Yemek Sepeti, Gitti Gidiyor, Markafoni and Peak Games to encourage and signal to everyone in the community that a very bright future can be real and achievable.

Seed capital with international mentorship and networking opportunities is the missing key element for our young local startups with global ambitions to succeed. This is why the Mini Seedcamp Istanbul event is very important for our ecosystem and why we’re very excited to be a part of this inaugural event.

So without further ado, below are the list of amazing startups that are selected to participate in the first Mini Seedcamp Istanbul:

Beware, they might just disrupt the market you are in.

Yalim K. Gerger Founder Formspider

Copyright © 2019 Seedcamp

Website design × Point Studio